Every passive income guru has a story. They started from nothing, built a system, and now earn $15,000 a month while working two hours a day from a beach somewhere warm. The screenshots look convincing. The timeline sounds fast. And the implication is always the same: you could do this too, starting today.

What they leave out is the math.

Not the aspirational math. Not the best-case-scenario math. The actual, grinding, compounding, slower-than-you-want-it-to-be math of building income that sustains itself without your daily involvement.

Because here’s the uncomfortable reality: passive income follows a mathematical curve that most people abandon before it starts paying off. The first six months are brutal. The first year is discouraging. The second year shows promise. And somewhere between year two and year five, the curve bends upward sharply enough that people finally understand why they should have started sooner.

This article runs the real numbers on every major passive income category. Not projections from someone selling a course. Actual math, with formulas you can verify, timelines you can plan around, and benchmarks that tell you whether you’re on track or falling behind.

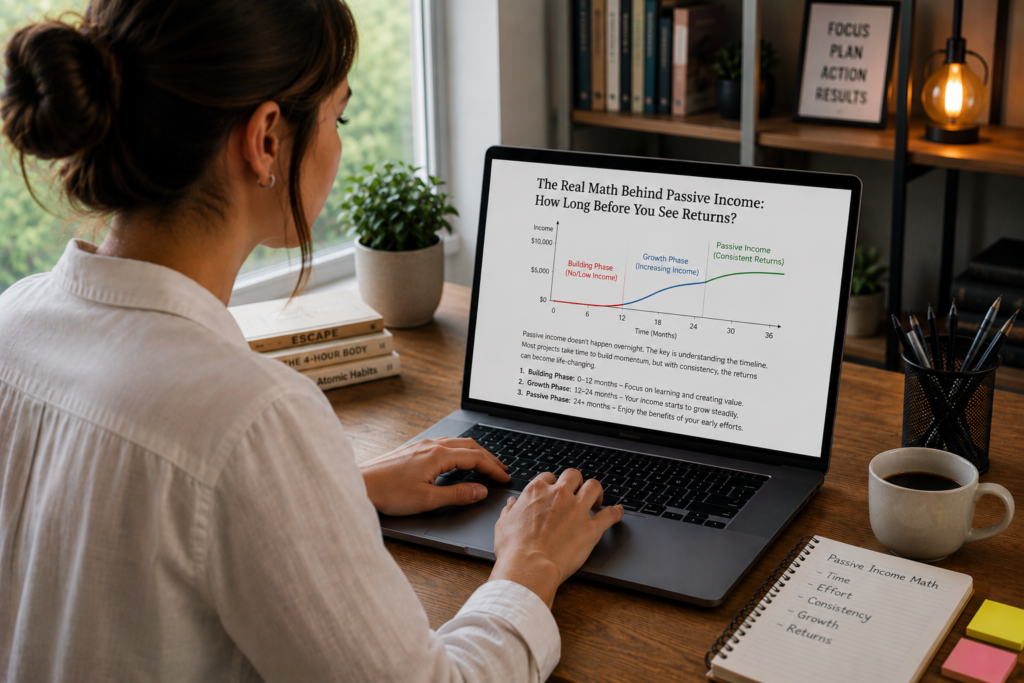

The Curve Nobody Shows You

Passive income growth doesn’t follow a straight line. It follows a curve that looks almost flat for a long time, then bends upward aggressively. Mathematicians call this exponential growth. Behavioral economists call it the reason people quit too early.

Here’s what the curve looks like in practice:

Months 1-6: You’re investing time, money, or both. Returns are negligible or zero. This phase feels like throwing effort into a void.

Months 7-12: Small returns begin to appear. A few dollars in dividends. A trickle of ad revenue. Your first digital product sale. The numbers are too small to matter financially, but they prove the system works.

Months 13-24: Growth accelerates modestly. Compounding begins to show. Your content library, investment balance, or product catalog reaches a size where the aggregate output becomes noticeable. You might hit $200-$500/month.

Months 25-48: The bend in the curve. Previous efforts compound on each other. Blog posts drive traffic to other blog posts. Dividends reinvest and generate their own dividends. Your reputation and audience create a flywheel. $1,000-$3,000/month becomes realistic.

Year 5 and beyond: The curve steepens dramatically. A portfolio that took four years to reach $100,000 might take only two more years to reach $200,000 (with continued contributions and reinvestment). A blog that took 18 months to reach 50,000 monthly pageviews might reach 150,000 in the following 12 months as domain authority compounds. This is where passive income starts feeling like the promise: meaningful money arriving with minimal ongoing effort.

The problem is that most people evaluate their progress at month 3 or month 6, see nearly nothing, and conclude it doesn’t work. They’re measuring a curve at the flattest part and extrapolating failure.

The Math of Investment-Based Passive Income

Investment-based passive income (savings accounts, dividends, REITs, bonds) follows the most predictable math because the formulas are well-established and the variables are knowable.

Compound Interest: The Formula That Runs Everything

The compound interest formula is:

$$A = P(1 + r/n)^{nt}$$

Where:

- A = Final amount

- P = Principal (starting investment)

- r = Annual interest rate (as a decimal)

- n = Number of times interest compounds per year

- t = Number of years

This formula tells you exactly what your money will grow to over any time period. No guessing. No speculation. Pure math.

Scenario 1: High-Yield Savings Account

Starting balance: $10,000

Monthly contribution: $500

APY: 4.5%

Compounding: Daily

| Year | Total Contributed | Account Balance | Interest Earned That Year | Cumulative Interest |

|---|---|---|---|---|

| 1 | $16,000 | $16,578 | $578 | $578 |

| 2 | $22,000 | $23,546 | $968 | $1,546 |

| 3 | $28,000 | $30,920 | $1,374 | $2,920 |

| 5 | $40,000 | $46,756 | $2,244 | $6,756 |

| 10 | $70,000 | $88,095 | $3,768 | $18,095 |

Time to $100/month in passive interest income: Approximately 2.5 years (when your balance reaches roughly $27,000 at 4.5% APY, you’re earning about $1,215/year or $101/month).

Time to $500/month: Approximately 8-9 years with consistent $500/month contributions, reaching a balance around $133,000.

The honest takeaway: High-yield savings produce meaningful passive income only with large balances. The math is reliable but slow. This is a wealth preservation and modest income tool, not a wealth creation engine.

Scenario 2: Dividend Investing with Reinvestment

Starting investment: $10,000

Monthly contribution: $500

Average dividend yield: 3.2%

Average annual stock price appreciation: 7%

Dividends reinvested: Yes

The total return (appreciation + dividends) averages around 10% annually for a diversified dividend portfolio over long periods, though individual years vary widely.

| Year | Total Contributed | Portfolio Value | Annual Dividends | Monthly Dividend Income (if not reinvested) |

|---|---|---|---|---|

| 1 | $16,000 | $17,200 | $550 | $46 |

| 2 | $22,000 | $25,320 | $810 | $68 |

| 3 | $28,000 | $34,450 | $1,102 | $92 |

| 5 | $40,000 | $55,800 | $1,786 | $149 |

| 10 | $70,000 | $131,500 | $4,208 | $351 |

| 15 | $100,000 | $243,600 | $7,795 | $650 |

| 20 | $130,000 | $407,200 | $13,030 | $1,086 |

Time to $100/month in dividend income: Approximately 3 years.

Time to $500/month: Approximately 12-13 years.

Time to $1,000/month: Approximately 18-20 years.

The honest takeaway: Dividend investing is a 15-20 year strategy for building meaningful monthly income. The math is powerful over long periods (your $130,000 in total contributions becomes $407,000+ after 20 years), but the early years produce frustratingly small dividends. The investor who starts at 25 and stays the course until 45 is in a completely different financial position than someone who waits until 35 to begin.

The Critical Variable: Starting Capital vs. Monthly Contributions

A common question: “Is it better to start with a large lump sum or make consistent monthly investments?”

The math answers this clearly.

Person A: Starts with $50,000, contributes $0/month

Person B: Starts with $0, contributes $500/month

Both invest in dividend-paying index funds averaging 10% annual total return.

| Year | Person A (Lump Sum) | Person B (Monthly) |

|---|---|---|

| 1 | $55,000 | $6,300 |

| 5 | $80,500 | $38,900 |

| 10 | $129,700 | $102,200 |

| 15 | $208,900 | $200,200 |

| 20 | $336,400 | $349,600 |

Person A leads for the first 14 years. Person B catches up around year 15 and pulls ahead after that, because their consistent contributions keep feeding the compounding engine while Person A’s pool grows only through returns.

The real lesson: The best approach is both. Start with whatever lump sum you can, then add consistent monthly contributions. But if you have to choose, consistent monthly investing beats a one-time investment over 15+ year horizons, which means you don’t need to wait until you have a large sum to start. Starting with $100/month right now beats waiting three years to invest $5,000.

The Rule of 72: A Quick Mental Shortcut

The Rule of 72 tells you approximately how many years it takes for your money to double at a given rate of return.

$$\text{Years to double} = 72 \div \text{annual return percentage}$$

| Annual Return | Years to Double |

|---|---|

| 4% | 18 years |

| 6% | 12 years |

| 8% | 9 years |

| 10% | 7.2 years |

| 12% | 6 years |

At 10% average annual returns, $10,000 becomes $20,000 in about 7 years, $40,000 in 14 years, and $80,000 in 21 years. Each doubling takes the same number of years, but the dollar amount of each doubling gets dramatically larger. The jump from $40,000 to $80,000 produces the same percentage return as the jump from $10,000 to $20,000, but it puts $40,000 in your pocket instead of $10,000.

This is why people who start investing in their 20s end up with dramatically more wealth than people who start in their 40s, even if the late starter invests more money per month. The early starter has more doublings ahead of them.

The Math of Content-Based Passive Income

Content-based income (blogs, YouTube, newsletters) follows different math than investment income. Instead of compound interest, you’re dealing with audience growth curves, content library effects, and revenue-per-unit metrics that improve over time.

Blog Math: Traffic, Revenue, and the Content Library Effect

A blog earns money primarily through display advertising (pay per pageview) and affiliate commissions (pay per conversion). Both scale directly with traffic, which scales with the number of quality posts and their search engine rankings.

Key metrics:

- RPM (Revenue Per Mille): How much you earn per 1,000 pageviews. Typical range: $15-$40 for display ads in most niches, with finance and business niches reaching $30-$60+.

- Affiliate conversion rate: The percentage of readers who click an affiliate link and buy. Typical range: 0.5-3% of pageviews, depending on content type and buying intent.

- Average monthly pageviews per post: A well-written, SEO-optimized blog post that ranks on Google might generate 200-2,000 pageviews per month once it reaches its ranking potential.

Blog Growth Timeline (Realistic Scenario)

Assumptions: One person writing 2 quality posts per week (8 per month). Posts average 800 monthly pageviews once ranked (which takes 3-8 months per post). Display ad RPM: $25. Modest affiliate revenue added.

| Month | Total Posts Published | Posts Ranked and Earning | Monthly Pageviews | Ad Revenue | Affiliate Revenue | Total Monthly Revenue |

|---|---|---|---|---|---|---|

| 3 | 24 | 4 | 3,200 | $80 | $15 | $95 |

| 6 | 48 | 15 | 12,000 | $300 | $90 | $390 |

| 9 | 72 | 30 | 24,000 | $600 | $200 | $800 |

| 12 | 96 | 50 | 40,000 | $1,000 | $400 | $1,400 |

| 18 | 144 | 85 | 68,000 | $1,700 | $750 | $2,450 |

| 24 | 192 | 130 | 104,000 | $2,600 | $1,200 | $3,800 |

Time to $100/month: Approximately 3 months.

Time to $1,000/month: Approximately 10-12 months.

Time to $3,000/month: Approximately 20-24 months.

The content library effect: Notice how the revenue accelerates even though the publishing pace stays constant. That’s because older posts continue to earn while new posts are added. By month 24, you have 192 posts, and about 130 of them are generating traffic every day without any additional work from you. Each new post you publish adds to an already-earning library.

This compounding of content is why blogs become increasingly passive over time. A blogger who published 200 posts over two years could stop writing entirely and continue earning $2,000-$3,000/month for months (gradually declining as posts age and competitors publish newer content, but far from dropping to zero overnight).

The Sobering Reality Check

The scenario above assumes every post is well-researched, well-written, SEO-optimized, and published consistently for 24 months straight. That’s 2 posts per week, 52 weeks, no breaks, no burnout, no extended vacations.

In practice:

- 30-40% of posts may never rank meaningfully

- Google algorithm updates can temporarily (or permanently) reduce traffic

- Consistency often breaks down around month 4-6 when early results are still small

- Niche selection dramatically affects RPM and traffic potential (a blog about luxury watches has different math than a blog about houseplant care)

Adjusted realistic expectation: If you account for inconsistent publishing, some posts that don’t perform, and a learning curve in the first few months, add 30-50% to the timelines above. Reaching $1,000/month in 14-16 months is a more honest benchmark for most new bloggers.

YouTube Math: Views, Watch Time, and the Algorithm Flywheel

YouTube monetization through the Partner Program pays based on ad impressions served during your videos. The metric that matters is RPM (revenue per 1,000 views after YouTube’s cut).

Typical YouTube RPM by niche:

| Niche | RPM Range |

|---|---|

| Personal finance, investing | $12-$35 |

| Business and entrepreneurship | $10-$25 |

| Technology and software | $8-$20 |

| Education and tutorials | $5-$15 |

| Health and fitness | $4-$12 |

| Entertainment and vlogging | $2-$8 |

| Gaming | $2-$6 |

YouTube growth timeline (realistic scenario):

Assumptions: Publishing 2 videos per week. Average production quality. Niche with moderate competition. RPM of $10.

| Month | Total Videos | Monthly Views | Monthly Ad Revenue | Sponsorship Revenue | Total Monthly Revenue |

|---|---|---|---|---|---|

| 3 | 24 | 2,000 | $20 | $0 | $20 |

| 6 | 48 | 8,000 | $80 | $0 | $80 |

| 9 | 72 | 20,000 | $200 | $0 | $200 |

| 12 | 96 | 45,000 | $450 | $200 | $650 |

| 18 | 144 | 100,000 | $1,000 | $600 | $1,600 |

| 24 | 192 | 200,000 | $2,000 | $1,500 | $3,500 |

Time to $100/month: Approximately 6-8 months.

Time to $1,000/month: Approximately 14-18 months.

Time to YouTube Partner Program eligibility (1,000 subscribers + 4,000 watch hours): Typically 6-12 months for a consistent creator.

The YouTube compounding effect: Similar to blogging, older videos continue generating views. A tutorial video you published 14 months ago might still get 300 views per day from YouTube search. Your video library becomes an asset that earns regardless of whether you uploaded anything this week.

The volatility factor: YouTube growth is less predictable than blog growth. A single video can go semi-viral (100,000+ views) and accelerate your channel by months. A string of underperforming videos can flatline your growth. The algorithm rewards consistency and watch time, but individual video performance is difficult to predict.

Newsletter Math: Subscribers, Open Rates, and Monetization

Newsletters monetize through three primary channels: sponsorships, paid subscriptions, and affiliate links.

Sponsorship rates (2025-2026 benchmarks):

| Subscriber Count | Typical Sponsorship Rate (per send) |

|---|---|

| 1,000-5,000 | $50-$200 |

| 5,000-10,000 | $200-$500 |

| 10,000-25,000 | $500-$1,500 |

| 25,000-50,000 | $1,500-$4,000 |

| 50,000-100,000 | $4,000-$10,000 |

Newsletter growth timeline (realistic scenario):

Assumptions: Publishing 2 newsletters per week. Solid niche with commercial appeal. Active promotion through social media and cross-promotions with other newsletters. Growing at 200-400 subscribers per month after the initial phase.

| Month | Total Subscribers | Monthly Sponsorship Revenue | Affiliate Revenue | Total Monthly Revenue |

|---|---|---|---|---|

| 3 | 600 | $0 | $20 | $20 |

| 6 | 1,800 | $100 | $60 | $160 |

| 9 | 3,500 | $250 | $120 | $370 |

| 12 | 5,500 | $500 | $200 | $700 |

| 18 | 10,000 | $1,200 | $400 | $1,600 |

| 24 | 16,000 | $2,500 | $700 | $3,200 |

Time to $100/month: Approximately 5-6 months.

Time to $1,000/month: Approximately 13-15 months.

Paid subscription model alternative: If you charge $10/month for a premium newsletter and convert 5% of your free subscribers to paid, 10,000 free subscribers yields 500 paid subscribers at $5,000/month. That math is compelling, but the 5% conversion rate requires genuinely differentiated content that readers can’t find anywhere else for free.

The Math of Digital Product Income

Digital products (templates, courses, printables, tools) follow a different curve because each product has a finite earning potential unless you continuously drive new traffic or create new products.

Single Digital Product Lifecycle

Most digital products follow a sales curve that looks like this:

Launch week: Spike in sales (especially if you have an existing audience). This might represent 20-40% of the product’s first-year revenue.

Months 1-3: Sales settle to a baseline level as launch excitement fades and organic discovery takes over.

Months 4-12: Steady, predictable sales driven by SEO, marketplace algorithms, and word of mouth. This is the “passive” phase.

Months 13-24: Gradual decline as competitors publish similar products and the market evolves. Updates and refreshes can extend this phase.

Year 3+: Long tail. Sales slow to a trickle but rarely reach zero if the product remains relevant and available.

Digital Product Revenue Model

Assumptions: A Notion template priced at $29 on Gumroad. No existing audience at launch. Marketing through SEO-optimized content and Pinterest.

| Month | Units Sold | Monthly Revenue | Cumulative Revenue |

|---|---|---|---|

| 1 (launch) | 8 | $232 | $232 |

| 2 | 5 | $145 | $377 |

| 3 | 6 | $174 | $551 |

| 6 | 10 | $290 | $1,421 |

| 9 | 14 | $406 | $2,639 |

| 12 | 18 | $522 | $4,373 |

Total first-year revenue from a single $29 product: approximately $4,000-$5,000 (with growing organic traffic and no paid advertising).

That’s decent for a product that took 30-40 hours to create. But it’s not life-changing. The math only becomes compelling when you build a catalog.

The Catalog Effect

| Number of Products | Average Monthly Revenue per Product | Total Monthly Revenue |

|---|---|---|

| 1 | $350 | $350 |

| 3 | $300 | $900 |

| 5 | $275 | $1,375 |

| 10 | $250 | $2,500 |

| 20 | $225 | $4,500 |

Revenue per product decreases slightly as you add more (attention and marketing effort get split), but total revenue grows steadily. A catalog of 10-20 digital products, built over 18-24 months, can produce $2,500-$5,000/month with modest ongoing maintenance.

Time to $500/month (single product): Approximately 8-12 months.

Time to $2,000/month (catalog approach): Approximately 18-24 months with consistent product creation (one new product every 4-6 weeks).

Online Course Revenue Model

Courses follow similar patterns but with higher price points and longer creation cycles.

Assumptions: A self-hosted course priced at $149. Small existing email list of 1,000 subscribers at launch. Marketing through content and email.

| Month | Units Sold | Monthly Revenue | Cumulative Revenue |

|---|---|---|---|

| 1 (launch) | 25 | $3,725 | $3,725 |

| 2 | 8 | $1,192 | $4,917 |

| 3 | 6 | $894 | $5,811 |

| 6 | 5 | $745 | $8,536 |

| 12 | 8 | $1,192 | $15,920 |

First-year revenue: approximately $14,000-$18,000 from a single course with modest marketing.

Time invested in creation: 80-120 hours.

Effective hourly rate: $14,000 ÷ 100 hours of creation + 50 hours of marketing = $93/hour in Year 1. And the course continues selling in Year 2 and beyond with minimal additional work.

The course model shines when your audience grows. The same course launched to a 10,000-person email list might sell 200 copies in launch week at $29,800 in revenue. Audience size is the multiplier that makes course math either mediocre or exceptional.

The Math of Real Estate Passive Income

Real estate follows its own mathematical logic, driven by leverage, appreciation, and cash flow.

The Leverage Advantage

Real estate is one of the few asset classes where you can control a large asset with a small amount of capital. A 20% down payment on a $300,000 property means you control $300,000 worth of real estate with $60,000.

If that property appreciates at 3% per year, the value increases by $9,000 in Year 1. On your $60,000 investment, that’s a 15% return on your money, even though the property itself only appreciated 3%.

This leverage works in both directions. If the property drops 10% in value ($30,000 decline), you’ve lost 50% of your $60,000 down payment on paper. Leverage magnifies gains and losses.

Rental Property Cash Flow Timeline

Assumptions: Purchase price $280,000. Down payment 20% ($56,000). 30-year mortgage at 6.8%. Monthly rent $1,900. Property tax $250/month. Insurance $110/month. Property management 10%. Maintenance reserve 10%. Vacancy reserve 5%.

| Line Item | Monthly |

|---|---|

| Rent collected | $1,900 |

| Mortgage (P&I) | -$1,098 |

| Property taxes | -$250 |

| Insurance | -$110 |

| Property management (10%) | -$190 |

| Maintenance reserve (10%) | -$190 |

| Vacancy reserve (5%) | -$95 |

| Monthly cash flow | -$33 |

Negative cash flow in Year 1. This is common in the current interest rate environment. But cash flow improves over time as rents increase while your mortgage payment stays fixed.

Cash flow projection with 3% annual rent increases:

| Year | Monthly Rent | Monthly Cash Flow |

|---|---|---|

| 1 | $1,900 | -$33 |

| 3 | $2,016 | +$83 |

| 5 | $2,138 | +$205 |

| 7 | $2,266 | +$333 |

| 10 | $2,476 | +$543 |

| 15 | $2,871 | +$938 |

| 20 | $3,328 | $1,395 |

Time to positive cash flow: Approximately 2 years.

Time to $500/month cash flow: Approximately 8-10 years.

Time to $1,000/month cash flow: Approximately 16-18 years.

These numbers look slow, but they tell only part of the story. During those 20 years:

Equity building through mortgage paydown:

| Year | Remaining Mortgage Balance | Equity from Paydown |

|---|---|---|

| 1 | $219,700 | $4,300 |

| 5 | $206,100 | $17,900 |

| 10 | $183,800 | $40,200 |

| 15 | $153,500 | $70,500 |

| 20 | $112,200 | $111,800 |

Appreciation (at 3% annual):

| Year | Property Value | Appreciation Gain |

|---|---|---|

| 5 | $324,600 | $44,600 |

| 10 | $376,200 | $96,200 |

| 15 | $436,100 | $156,100 |

| 20 | $505,600 | $225,600 |

Total return after 20 years:

| Component | Value |

|---|---|

| Cash flow collected (cumulative, net) | ~$72,000 |

| Equity from mortgage paydown | $111,800 |

| Appreciation | $225,600 |

| Tax benefits (estimated, varies widely) | $30,000-$50,000 |

| Total return on $56,000 down payment | ~$440,000-$460,000 |

That’s roughly an 8x return on your initial investment over 20 years, or about 11% annualized. And once the mortgage is paid off (Year 30), the monthly cash flow jumps to roughly $2,500-$3,000/month (rent minus taxes, insurance, management, and maintenance), since the largest expense (the mortgage) disappears entirely.

The honest takeaway: Rental property is a 10-30 year passive income play. The early years are break-even or slightly negative on cash flow. The wealth builds silently through equity and appreciation. The truly passive income phase begins when the mortgage is paid off or when rents have grown significantly above your fixed mortgage payment.

Comparing Timelines Across All Streams

Here’s every major passive income stream, side by side, with honest timelines to specific income milestones.

Time to $100/month:

| Stream | Time Required | Upfront Cost |

|---|---|---|

| High-yield savings | Immediate (with ~$27,000 deposited) | $27,000 |

| Dividend investing | 2-3 years (with $500/month contributions) | $10,000+ |

| Blog | 3-4 months | $100-$300 |

| YouTube | 6-8 months | $200-$500 |

| Newsletter | 5-6 months | $0-$50 |

| Digital products | 2-4 months | $50-$200 |

| Online course | 2-3 months (with existing audience) | $200-$500 |

| Rental property | 2-3 years (cash flow) | $50,000+ |

Time to $1,000/month:

| Stream | Time Required | Cumulative Investment |

|---|---|---|

| High-yield savings | Immediate (with ~$267,000) | $267,000 |

| Dividend investing | 8-10 years | $50,000-$80,000 contributed |

| Blog | 10-16 months | $500-$2,000 + 500-800 hours |

| YouTube | 14-20 months | $500-$2,000 + 600-1,000 hours |

| Newsletter | 13-18 months | $200-$1,000 + 400-600 hours |

| Digital products | 12-18 months (catalog) | $200-$500 + 300-500 hours |

| Online course | 6-12 months (with audience) | $500-$2,000 + 150-300 hours |

| Rental property | 8-10 years | $60,000-$100,000 |

Time to $5,000/month:

| Stream | Time Required | Cumulative Investment |

|---|---|---|

| High-yield savings | Immediate (with ~$1.33 million) | $1,330,000 |

| Dividend investing | 15-20 years | $130,000+ contributed |

| Blog | 24-36 months | $2,000-$5,000 + 1,500-2,500 hours |

| YouTube | 24-36 months | $2,000-$5,000 + 1,500-2,500 hours |

| Newsletter | 24-36 months | $1,000-$3,000 + 1,000-1,500 hours |

| Digital products | 24-36 months (large catalog) | $1,000-$3,000 + 800-1,500 hours |

| Online course | 18-30 months (with growing audience) | $2,000-$5,000 + 500-1,000 hours |

| Rental property | 15-20 years (or multiple properties) | $150,000-$300,000 |

The Hidden Variable: Your Hourly Rate During the Building Phase

One calculation that passive income advocates conveniently skip is the effective hourly rate during the building phase. This number is humbling, and it’s worth confronting honestly.

Blog example

You spend 800 hours over 12 months building a blog. In month 12, you’re earning $1,400/month. But your total earnings for the year (summing each month’s growing revenue) might be $5,000-$6,000.

Effective hourly rate for Year 1: $5,500 ÷ 800 hours = $6.88/hour

That’s below minimum wage. If you’re evaluating the blog purely as a Year 1 income proposition, it’s a terrible deal. You could earn more per hour flipping burgers.

But in Year 2, you might earn $25,000-$35,000 from the blog while investing only 400 hours (maintaining and publishing at a reduced pace).

Effective hourly rate for Year 2: $30,000 ÷ 400 hours = $75/hour

And in Year 3, if the blog is mature and you’re mostly maintaining: $35,000-$45,000 from 200 hours of work.

Effective hourly rate for Year 3: $40,000 ÷ 200 hours = $200/hour

The pattern is clear: early hours are massively undercompensated, and later hours are massively overcompensated. The question is whether you can tolerate the underpayment long enough to reach the overpayment phase.

Digital product example

You spend 40 hours creating a digital product. In its first year, it earns $4,500.

Effective hourly rate: $4,500 ÷ 40 hours = $112.50/hour

In Year 2, the product earns $3,000 with 5 hours of maintenance.

Year 2 hourly rate: $3,000 ÷ 5 hours = $600/hour

Digital products tend to reach a favorable hourly rate faster than content businesses because the creation time is concentrated and the earning period extends for years.

The cumulative hourly rate perspective

The most useful way to evaluate passive income is a cumulative hourly rate that spans the entire history of the project.

Blog, cumulative over 3 years:

Total revenue: $5,500 (Year 1) + $30,000 (Year 2) + $40,000 (Year 3) = $75,500

Total hours: 800 (Year 1) + 400 (Year 2) + 200 (Year 3) = 1,400 hours

Cumulative rate: $53.93/hour

And that rate keeps improving every year that the blog continues earning. By Year 5, the cumulative rate might be $80-$100/hour, with the ongoing hourly rate well above $200/hour.

This long-view perspective is the financial argument for building passive income. You’re not doing it for the immediate return. You’re doing it because the per-hour return improves every year, eventually exceeding what you could earn trading time for money at any job.

The Break-Even Calculation: When Does Passive Income Justify Its Cost?

Every passive income project has a break-even point: the moment when total earnings exceed total costs (time valued at your opportunity cost, plus any money invested).

How to calculate your break-even point

Step 1: Determine your opportunity cost per hour. This is what you could earn doing something else with the same time. If your day job pays $40/hour, that’s your opportunity cost.

Step 2: Calculate total hours invested in your passive income project.

Step 3: Add any direct financial costs (hosting, tools, equipment, investment capital).

Step 4: Total cost = (hours × opportunity cost) + direct costs.

Step 5: Track cumulative revenue. When revenue exceeds total cost, you’ve broken even.

Break-even example: Blog

- Opportunity cost: $40/hour

- Year 1 hours: 800

- Direct costs: $500 (hosting, tools)

- Total cost after Year 1: (800 × $40) + $500 = $32,500

- Year 1 revenue: $5,500

- Year 1 deficit: $27,000

- Year 2 hours: 400

- Additional costs: $300

- Cumulative cost after Year 2: $32,500 + (400 × $40) + $300 = $48,800

- Cumulative revenue after Year 2: $5,500 + $30,000 = $35,500

- Year 2 deficit: $13,300

- Year 3 hours: 200

- Additional costs: $300

- Cumulative cost after Year 3: $48,800 + (200 × $40) + $300 = $57,100

- Cumulative revenue after Year 3: $35,500 + $40,000 = $75,500

- Year 3 surplus: $18,400 (break-even occurred partway through Year 3)

Break-even point: approximately 28-30 months.

After break-even, every additional dollar of revenue is profit on top of what you could have earned doing something else with that time. This is when passive income genuinely starts to “work.”

Break-even example: Dividend portfolio

- Opportunity cost of capital: If you could earn 4.5% in a high-yield savings account with zero effort, that’s your baseline. Dividend investing needs to beat that return to justify the additional complexity and risk.

- With average total returns of 10% and savings account returns of 4.5%, the incremental return is 5.5%.

- On a $50,000 portfolio, that’s $2,750/year in returns above what a savings account would generate.

- The break-even question becomes: Is $2,750/year in additional returns (plus the potential for much higher returns through stock appreciation) worth the risk of market volatility and the time spent managing the portfolio?

For most people, the answer is yes over long time periods. The stock market has outperformed savings accounts over every 20+ year period in history. But the break-even framing helps you understand that the benefit of investing over saving is incremental, not transformational, in the short term.

The One Number That Predicts Success

Across every passive income stream, one metric predicts success better than any other: consistency measured in months, not effort measured in hours.

A blogger who publishes one post per week for 24 months will almost certainly outperform a blogger who publishes five posts per week for 4 months and then burns out.

An investor who contributes $300/month for 15 years will almost certainly outperform an investor who contributes $1,500/month for 2 years and then stops.

A digital product creator who launches one new product every six weeks for two years will almost certainly outperform someone who launches five products in a single month and then moves on to something else.

The math rewards duration more than intensity. Compounding, whether financial compounding or content library compounding, needs time to work. Intensity without duration produces a spike followed by a cliff. Duration with moderate intensity produces a curve that bends upward and stays there.

If you take nothing else from this article, take this: the timeline to meaningful passive income is measured in years, not months. But within that timeline, the returns accelerate rather than plateau. You earn more per unit of effort in Year 3 than Year 2, more in Year 5 than Year 3, and more in Year 10 than Year 5.

The math is on your side. But only if you stay long enough to let it work.

Running Your Own Numbers

Generic projections are useful for setting expectations, but your specific situation has its own variables. Here’s how to build a personalized timeline.

For investment-based income:

- Determine your starting capital and monthly contribution capacity.

- Choose a realistic annual return (4-5% for savings, 7-10% for diversified stock/dividend portfolios, 3-6% for REITs).

- Use a compound interest calculator (every major financial website has one) to project your balance over 5, 10, 15, and 20 years.

- Multiply projected balances by your expected yield (dividend yield for stocks, interest rate for savings) to estimate monthly income at each milestone.

For content-based income:

- Determine your realistic publishing pace (posts per week, videos per week, newsletters per week).

- Estimate average monthly traffic per piece of content after it matures (use competitors’ traffic as a benchmark if possible, tools like Ahrefs or Semrush can estimate this).

- Multiply: (number of published pieces × average traffic per piece × RPM/1,000) = estimated monthly revenue.

- Plot this monthly for 24 months, accounting for the delay between publishing and ranking (typically 3-8 months for blog posts).

For digital products:

- Estimate units sold per month per product after launch stabilization (be conservative: 5-20 units/month for a $20-$50 product without a large existing audience).

- Multiply by price to get monthly revenue per product.

- Determine your product creation pace (one every 4-8 weeks is sustainable for most solo creators).

- Project monthly revenue as your catalog grows over 12, 18, and 24 months.

Write these projections down. Check them against reality every quarter. Adjust the inputs based on actual performance, not based on what you wish would happen. The math doesn’t lie, but your assumptions might.

The Honest Conclusion

Passive income is real. The math is real. The returns are real. And the timeline is longer than almost anyone wants to hear.

The investors who earn $3,000/month in dividends built portfolios over 15-20 years. The bloggers earning $5,000/month published consistently for 2-3 years. The digital product creators earning $4,000/month built catalogs of 15-20 products over 18-24 months. The rental property owners collecting $2,000/month in cash flow bought their properties a decade ago and held through market cycles, tenant headaches, and maintenance expenses.

None of them got there in 90 days. All of them got there by understanding the math, trusting the curve, and showing up consistently during the long, flat, unimpressive early phase where the numbers barely moved.

The math is the same for you. The formulas don’t care about your background, your starting capital, or your follower count. They care about inputs (money invested, content published, products created) and time. Provide enough of both, and the outputs follow with mechanical reliability.

The only remaining question is the one no formula can answer: will you stay in the game long enough for the math to do its work?