Introduction

Budgeting and money management are essential skills that can significantly impact your financial well-being. Whether you’re trying to save more money, pay off debt, build wealth, or simply gain better control over your finances, having a solid budgeting strategy is the foundation of long-term financial success.

Many people struggle with managing their income because they lack a clear plan for where their money goes each month. Without a budget, it becomes easy to overspend, accumulate debt, and fall short of financial goals. Fortunately, effective money management doesn’t require a high income—it requires discipline, planning, and consistency.

In this comprehensive guide, you’ll learn practical budgeting techniques, money management strategies, and financial habits that can help you take control of your finances and create a secure future.

What Is Budgeting?

Budgeting is the process of creating a plan for your income and expenses. It helps you allocate money toward necessities, savings, debt repayment, and personal goals.

A budget serves as a financial roadmap, allowing you to:

- Monitor spending habits

- Avoid unnecessary debt

- Increase savings

- Prepare for emergencies

- Achieve financial goals

- Reduce financial stress

A well-designed budget ensures that every dollar has a purpose.

Why Money Management Is Important

Money management goes beyond budgeting. It involves making informed decisions about earning, spending, saving, investing, and protecting your money.

Effective money management can help you:

Build Financial Security

Having control over your finances provides stability during unexpected situations such as job loss, medical emergencies, or economic downturns.

Reduce Stress

Financial uncertainty is a major source of anxiety. Proper planning helps eliminate many money-related concerns.

Achieve Financial Goals

Whether you want to buy a home, travel, start a business, or retire comfortably, good money management makes these goals achievable.

Increase Wealth

Strategic saving and investing allow your money to grow over time through compound returns.

Step 1: Understand Your Income

The first step in budgeting is knowing exactly how much money you earn each month.

Sources of income may include:

- Salary or wages

- Freelance work

- Side businesses

- Rental income

- Investment income

- Bonuses and commissions

Focus on your net income (after taxes and deductions), as this represents the actual amount available for spending and saving.

Step 2: Track Your Expenses

Before creating a budget, it’s important to understand where your money is currently going.

Common expense categories include:

Fixed Expenses

These remain relatively consistent each month:

- Rent or mortgage

- Insurance

- Loan payments

- Utilities

- Internet and phone bills

Variable Expenses

These fluctuate monthly:

- Groceries

- Entertainment

- Dining out

- Transportation

- Shopping

Tracking expenses for at least 30 days can reveal spending patterns and identify areas where costs can be reduced.

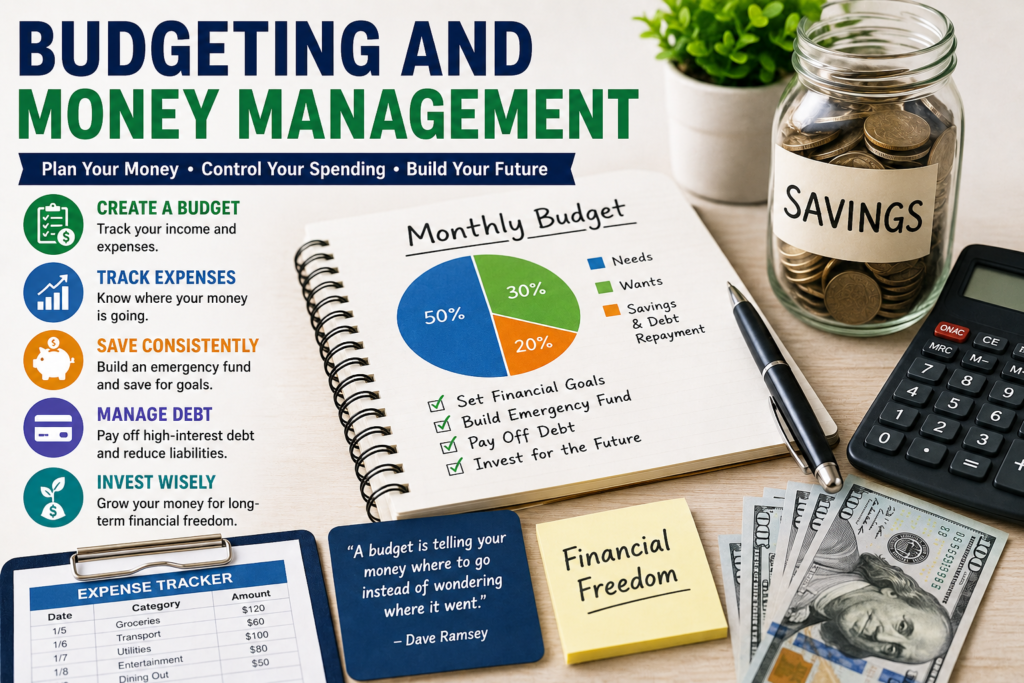

Step 3: Create a Monthly Budget

A monthly budget helps allocate income effectively.

The 50/30/20 Rule

One of the most popular budgeting methods is the 50/30/20 rule:

50% Needs

Essential expenses such as:

- Housing

- Utilities

- Food

- Transportation

- Insurance

30% Wants

Non-essential spending including:

- Entertainment

- Hobbies

- Dining out

- Vacations

20% Savings and Debt Repayment

Money allocated toward:

- Emergency savings

- Retirement accounts

- Investments

- Extra debt payments

This method provides a simple framework for maintaining financial balance.

Step 4: Set Clear Financial Goals

Successful budgeting requires clear objectives.

Short-Term Goals

Achievable within one year:

- Build a $1,000 emergency fund

- Pay off a credit card

- Save for a vacation

Medium-Term Goals

Typically one to five years:

- Purchase a car

- Save for a home down payment

- Start a business

Long-Term Goals

More than five years:

- Retirement planning

- Financial independence

- College savings

Goals help maintain motivation and provide direction for financial decisions.

Step 5: Build an Emergency Fund

An emergency fund protects against unexpected expenses and financial setbacks.

Examples include:

- Medical bills

- Car repairs

- Home maintenance

- Job loss

Financial experts generally recommend saving three to six months of living expenses.

Benefits of an emergency fund include:

- Reduced reliance on credit cards

- Lower financial stress

- Greater financial flexibility

Even small contributions can add up significantly over time.

Step 6: Eliminate Debt Strategically

Debt can limit financial growth and reduce available income for savings and investments.

Common Types of Debt

- Credit card debt

- Student loans

- Auto loans

- Personal loans

- Mortgages

Debt Snowball Method

Focus on paying off the smallest balance first while making minimum payments on other debts.

Advantages:

- Quick psychological wins

- Increased motivation

Debt Avalanche Method

Pay debts with the highest interest rates first.

Advantages:

- Lower total interest costs

- Faster long-term debt reduction

Choose the strategy that best matches your financial personality and goals.

Step 7: Increase Savings

Saving money is a critical component of financial success.

Automate Savings

Set up automatic transfers to savings accounts immediately after receiving income.

Reduce Unnecessary Expenses

Examples include:

- Cancel unused subscriptions

- Cook meals at home

- Compare insurance rates

- Use shopping lists

- Limit impulse purchases

Save Windfalls

Consider saving:

- Tax refunds

- Bonuses

- Gifts

- Extra income

These funds can significantly accelerate savings goals.

Step 8: Improve Spending Habits

Smart spending is one of the most effective money management skills.

Differentiate Needs and Wants

Before making purchases, ask:

- Is this necessary?

- Can it wait?

- Does it align with my financial goals?

Practice Delayed Gratification

Waiting 24 to 48 hours before making large purchases can reduce impulse spending and buyer’s remorse.

Shop Intentionally

Compare prices, use discounts, and prioritize value over impulse.

Step 9: Invest for the Future

Investing helps your money grow faster than traditional savings accounts.

Popular investment options include:

- Stocks

- Bonds

- ETFs

- Mutual funds

- Real estate

- Retirement accounts

Benefits of Investing

- Long-term wealth growth

- Protection against inflation

- Potential passive income

Starting early allows compound growth to work in your favor.

Step 10: Review Your Budget Regularly

Budgets should evolve with your financial circumstances.

Review your budget monthly to:

- Track progress

- Adjust spending categories

- Update financial goals

- Identify improvement opportunities

Regular reviews help maintain accountability and financial discipline.

Common Budgeting Mistakes to Avoid

Many people struggle because of avoidable budgeting errors.

Not Tracking Expenses

Ignoring spending habits often leads to overspending.

Setting Unrealistic Budgets

Overly restrictive budgets are difficult to maintain long term.

Forgetting Irregular Expenses

Include annual costs such as:

- Insurance premiums

- Vehicle maintenance

- Holiday spending

Ignoring Savings

Savings should be treated as a mandatory expense, not an optional one.

Failing to Adjust

Life circumstances change, and budgets should adapt accordingly.

Best Tools for Budgeting and Money Management

Modern technology makes budgeting easier than ever.

Popular tools include:

- Budgeting apps

- Expense tracking software

- Spreadsheet templates

- Online banking tools

- Financial planning platforms

The best tool is the one you’ll consistently use.

Money Management Habits of Financially Successful People

Highly successful individuals often share common financial habits:

- They live below their means.

- They maintain a budget.

- They save consistently.

- They avoid high-interest debt.

- They invest regularly.

- They track financial progress.

- They continue learning about personal finance.

These habits create a strong foundation for long-term financial success.

How Budgeting Leads to Financial Freedom

Financial freedom means having enough resources to support your desired lifestyle without constant financial stress.

Budgeting contributes to financial freedom by:

- Increasing savings

- Reducing debt

- Improving spending decisions

- Supporting investment growth

- Creating financial stability

The sooner you develop strong money management habits, the sooner you’ll move toward financial independence.

Conclusion

Budgeting and money management are not about restricting your lifestyle—they are about creating a plan that allows you to use your money effectively and intentionally.

By tracking expenses, creating a realistic budget, building emergency savings, eliminating debt, investing consistently, and reviewing your progress regularly, you can dramatically improve your financial health.

Remember that financial success is built through small, consistent actions over time. Start with a simple budget, stay committed to your goals, and continue refining your money management skills. Over the long term, these habits can help you achieve financial security, wealth, and lasting peace of mind.