Introduction

Debt can be one of the biggest obstacles to financial stability and long-term wealth building. Whether it’s credit card balances, personal loans, student loans, or other financial obligations, excessive debt can create stress, limit financial opportunities, and reduce your ability to save and invest.

The good news is that with the right debt reduction methods, you can take control of your finances and work toward becoming debt-free. Successful debt management requires discipline, planning, and a clear repayment strategy.

In this guide, you’ll learn the most effective debt reduction techniques, practical money-saving strategies, and proven methods that can help you eliminate debt faster and improve your financial future.

Why Debt Reduction Matters

Reducing debt provides numerous financial and personal benefits:

Improved Cash Flow

Less debt means more money available for:

- Savings

- Investments

- Emergency funds

- Lifestyle goals

Reduced Financial Stress

Lower debt levels often lead to greater peace of mind and financial confidence.

Better Credit Scores

Consistent debt repayment can improve your credit profile and borrowing opportunities.

Increased Financial Freedom

Becoming debt-free creates opportunities to focus on wealth building rather than debt payments.

Understanding Good Debt vs. Bad Debt

Not all debt is created equal.

Good Debt

Good debt may help increase future income or net worth.

Examples include:

- Education loans

- Business loans

- Reasonable mortgage debt

Bad Debt

Bad debt typically finances depreciating assets or unnecessary spending.

Examples include:

- High-interest credit cards

- Payday loans

- Consumer debt

- Excessive personal loans

Reducing high-interest debt should usually be your top priority.

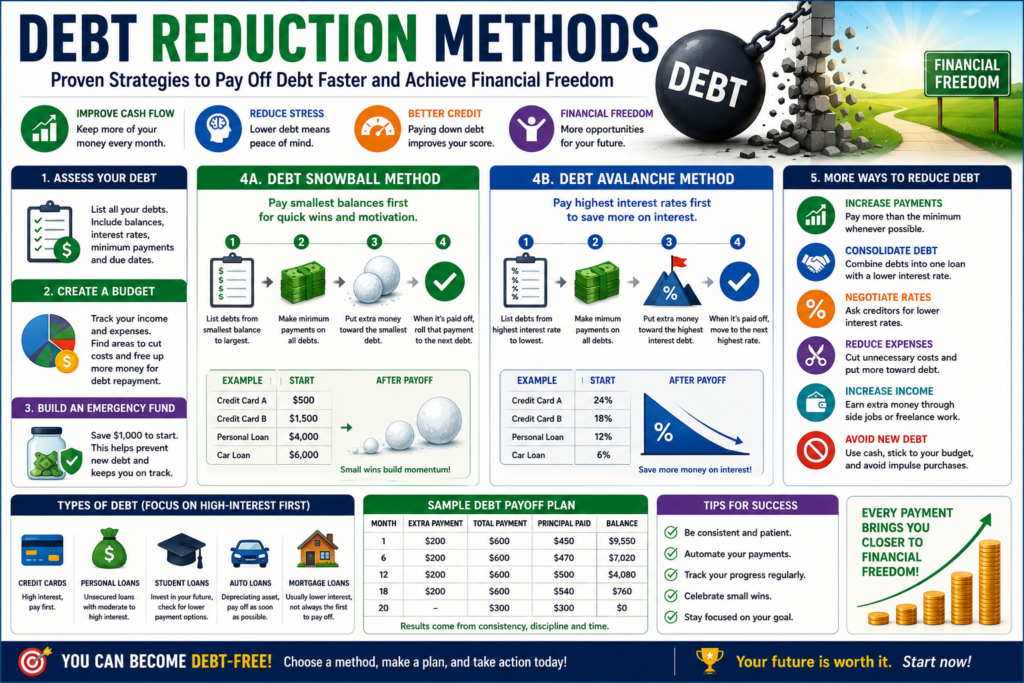

Step 1: Assess Your Debt Situation

Begin by creating a complete list of all debts.

Include:

- Creditor names

- Outstanding balances

- Interest rates

- Minimum monthly payments

- Due dates

Understanding your debt picture allows you to create a realistic repayment plan.

Step 2: Create a Debt Repayment Budget

A budget is essential for successful debt reduction.

Track:

- Monthly income

- Fixed expenses

- Variable expenses

- Debt payments

Identify areas where spending can be reduced and redirect those savings toward debt repayment.

Step 3: Use the Debt Snowball Method

The Debt Snowball Method focuses on paying off the smallest balances first.

How It Works

- List debts from smallest to largest balance.

- Make minimum payments on all debts.

- Put extra money toward the smallest debt.

- Once paid off, roll that payment into the next debt.

Advantages

- Quick wins

- Increased motivation

- Simple implementation

Many people find this method psychologically rewarding.

Step 4: Use the Debt Avalanche Method

The Debt Avalanche Method prioritizes debts with the highest interest rates.

How It Works

- Rank debts by interest rate.

- Make minimum payments on all debts.

- Apply extra funds to the highest-interest debt.

- Continue until all debts are eliminated.

Advantages

- Saves more money on interest

- Faster overall debt reduction

- Mathematically efficient

This strategy often results in the lowest total repayment cost.

Step 5: Increase Monthly Payments

Paying more than the minimum payment can dramatically reduce repayment time.

Benefits include:

- Faster debt elimination

- Lower interest costs

- Improved cash flow sooner

Even modest additional payments can make a significant difference.

Step 6: Consolidate Debt

Debt consolidation combines multiple debts into a single payment.

Potential benefits:

- Simplified finances

- Lower interest rates

- Fixed repayment schedules

Common consolidation options include:

- Personal loans

- Balance transfer cards

- Home equity loans

Always compare fees and terms before consolidating.

Step 7: Negotiate Lower Interest Rates

Many creditors may be willing to reduce interest rates for reliable customers.

Benefits include:

- Lower monthly payments

- Reduced total interest

- Faster payoff timelines

A simple phone call could save hundreds or even thousands of dollars.

Step 8: Reduce Unnecessary Expenses

Every dollar saved can be redirected toward debt repayment.

Consider reducing:

- Subscription services

- Dining out

- Entertainment expenses

- Impulse purchases

- Luxury spending

Temporary sacrifices can accelerate long-term financial freedom.

Step 9: Increase Your Income

Additional income can significantly speed up debt repayment.

Options include:

- Freelancing

- Side businesses

- Overtime work

- Selling unused items

- Consulting services

Using extra income exclusively for debt reduction can produce rapid results.

Step 10: Avoid Accumulating New Debt

One of the most important debt reduction principles is preventing new debt.

Strategies include:

- Using cash when possible

- Following a budget

- Building an emergency fund

- Avoiding impulse purchases

Debt reduction becomes much easier when balances stop growing.

Debt Reduction Through Emergency Savings

Many people focus entirely on debt repayment and neglect savings.

Maintaining a small emergency fund helps prevent:

- New credit card balances

- Unexpected borrowing

- Financial setbacks

A starter emergency fund of $1,000 can provide valuable protection.

Common Debt Reduction Mistakes

Avoid these common errors:

Paying Only Minimum Payments

Minimum payments often keep debt around for years.

Ignoring High Interest Rates

High-interest debt can significantly increase total repayment costs.

Not Following a Budget

Without a spending plan, debt reduction efforts may stall.

Closing All Credit Accounts Immediately

Closing accounts can sometimes negatively affect credit utilization ratios.

Taking on New Debt

New debt can undo months of repayment progress.

Debt Reduction Timeline Example

Credit Card Debt: $10,000

Minimum Payment Only:

- May take many years

- Thousands in interest

Extra $200 Monthly:

- Faster payoff

- Significant interest savings

Consistency is often more important than the size of individual payments.

Best Habits for Becoming Debt-Free

Successful debt reducers typically:

- Track spending carefully

- Follow a budget

- Make payments on time

- Avoid unnecessary borrowing

- Increase income when possible

- Review financial progress regularly

These habits support long-term financial health.

Life After Debt

Becoming debt-free opens opportunities to:

- Build emergency savings

- Invest for retirement

- Purchase a home

- Start a business

- Achieve financial independence

Many people experience improved financial confidence and reduced stress after eliminating debt.

Conclusion

Debt reduction is a journey that requires patience, discipline, and commitment. Whether you choose the Debt Snowball Method, Debt Avalanche Method, debt consolidation, or a combination of strategies, the most important factor is taking consistent action.

By creating a budget, increasing payments, reducing expenses, avoiding new debt, and staying focused on your goals, you can steadily eliminate debt and build a stronger financial future.

Every payment brings you one step closer to financial freedom. Start today, stay consistent, and remember that lasting financial success is built through small, disciplined actions over time.