Introduction

Retirement planning is one of the most important financial goals you’ll ever pursue. A well-structured retirement plan helps ensure you can maintain your desired lifestyle, cover healthcare expenses, and enjoy financial independence during your retirement years.

Many people delay retirement planning because it feels distant or overwhelming. However, the earlier you start, the easier it becomes to build a substantial retirement fund through the power of compound growth.

Whether you’re just beginning your career or approaching retirement age, understanding retirement planning strategies can help you create a secure and comfortable future.

What Is Retirement Planning?

Retirement planning is the process of preparing financially for life after full-time employment.

It involves:

- Setting retirement goals

- Estimating future expenses

- Building retirement savings

- Investing for long-term growth

- Managing retirement risks

- Creating income streams for retirement

The goal is to ensure your savings and investments can support your lifestyle throughout retirement.

Why Retirement Planning Matters

Retirement planning provides several important benefits:

Financial Independence

A strong retirement plan reduces dependence on family members or government assistance.

Lifestyle Security

Planning helps maintain your preferred standard of living after retirement.

Healthcare Preparedness

Medical expenses often increase with age, making financial preparation essential.

Peace of Mind

Knowing you’re financially prepared can reduce stress and uncertainty about the future.

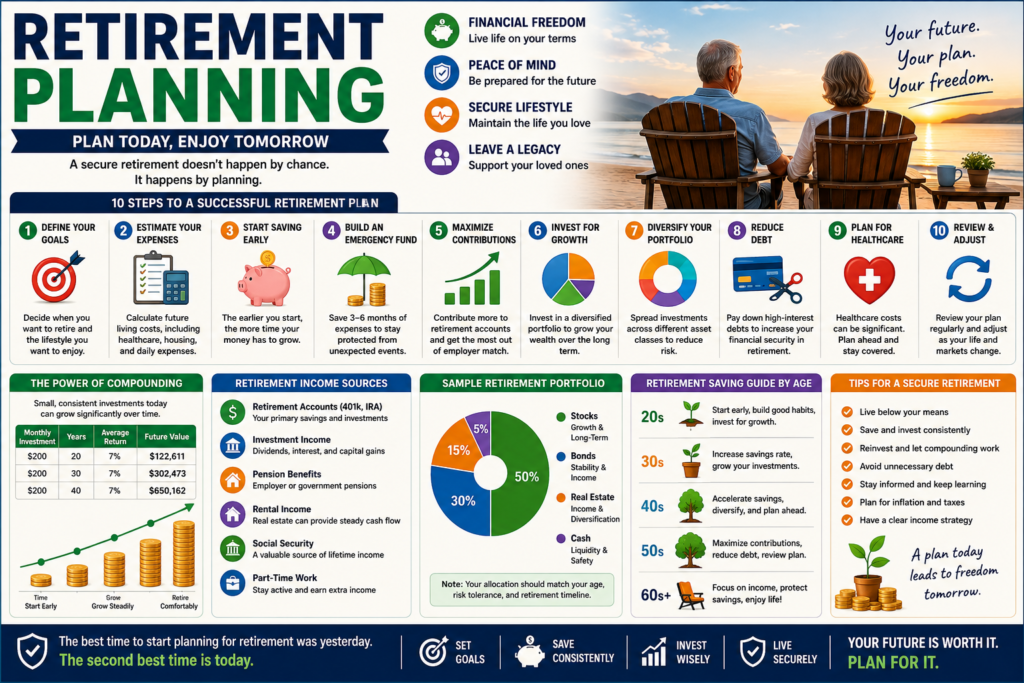

Step 1: Define Your Retirement Goals

Every retirement plan should begin with clear objectives.

Consider:

- Desired retirement age

- Preferred lifestyle

- Travel plans

- Housing needs

- Healthcare expectations

- Family support responsibilities

The more specific your goals, the more effective your retirement strategy will be.

Step 2: Estimate Retirement Expenses

Understanding future expenses helps determine how much money you’ll need.

Common retirement costs include:

Housing

- Mortgage payments

- Property taxes

- Maintenance

- Utilities

Healthcare

- Insurance premiums

- Medications

- Medical treatments

- Long-term care

Daily Living Expenses

- Food

- Transportation

- Entertainment

- Travel

Many financial experts estimate retirees need approximately 70%–90% of their pre-retirement income annually.

Step 3: Start Saving Early

Time is one of the most valuable assets in retirement planning.

Benefits of starting early:

- Greater compound growth

- Lower monthly contribution requirements

- Increased flexibility

- Larger retirement balances

Even small monthly contributions can grow substantially over several decades.

Step 4: Build an Emergency Fund

Before focusing heavily on retirement investing, establish an emergency fund.

Financial experts typically recommend:

- Three to six months of living expenses

- Easily accessible savings

- Protection against unexpected events

This prevents retirement investments from being withdrawn prematurely.

Step 5: Maximize Retirement Contributions

Consistent contributions are critical for retirement success.

Strategies include:

- Increasing contributions annually

- Contributing after salary raises

- Automating retirement deposits

- Taking advantage of employer matching programs

Small increases over time can significantly impact retirement wealth.

Step 6: Invest for Long-Term Growth

Retirement investing focuses on long-term wealth accumulation.

Popular investment options include:

Stocks

Benefits:

- High growth potential

- Inflation protection

Risks:

- Market volatility

Bonds

Benefits:

- Lower risk

- Income generation

Risks:

- Lower long-term returns

Index Funds

Benefits:

- Diversification

- Low fees

- Simplicity

Many retirement portfolios use index funds as a core investment.

Exchange-Traded Funds (ETFs)

Benefits:

- Flexibility

- Diversification

- Cost efficiency

Step 7: Diversify Your Retirement Portfolio

Diversification reduces investment risk.

A diversified retirement portfolio may include:

- Domestic stocks

- International stocks

- Bonds

- Real estate investments

- Cash reserves

Diversification helps protect against market fluctuations and economic uncertainty.

Step 8: Understand the Power of Compound Growth

Compound growth allows investment earnings to generate additional earnings over time.

Key factors include:

- Time

- Consistency

- Reinvestment

The longer investments remain invested, the greater the potential growth.

Step 9: Reduce Debt Before Retirement

Entering retirement with significant debt can strain finances.

Prioritize paying off:

- Credit cards

- Personal loans

- Auto loans

- High-interest debt

Reducing debt improves cash flow and financial flexibility during retirement.

Step 10: Plan for Healthcare Costs

Healthcare is often one of the largest retirement expenses.

Potential costs include:

- Insurance premiums

- Prescription medications

- Specialist care

- Long-term care services

Including healthcare expenses in retirement planning is essential.

Common Retirement Planning Mistakes

Avoid these common errors:

Starting Too Late

Delaying retirement savings reduces the benefits of compound growth.

Underestimating Expenses

Many retirees spend more than expected, particularly on healthcare and leisure activities.

Insufficient Diversification

Overconcentration increases investment risk.

Withdrawing Funds Early

Early withdrawals can reduce long-term retirement security.

Ignoring Inflation

Inflation gradually reduces purchasing power over time.

Retirement Planning by Age

In Your 20s

Focus on:

- Building savings habits

- Starting investments early

- Taking advantage of compound growth

In Your 30s

Prioritize:

- Increasing contributions

- Expanding investments

- Reducing debt

In Your 40s

Focus on:

- Accelerating retirement savings

- Reviewing investment allocations

- Refining retirement goals

In Your 50s

Emphasize:

- Maximizing retirement contributions

- Reducing financial risks

- Finalizing retirement strategies

In Your 60s

Prepare for:

- Retirement income planning

- Portfolio adjustments

- Healthcare planning

Retirement Income Sources

Successful retirees often rely on multiple income streams.

Potential sources include:

- Retirement accounts

- Investment portfolios

- Pension benefits

- Rental income

- Dividend income

- Part-time work

- Government retirement benefits

Diversified income sources provide greater financial stability.

Building a Retirement Mindset

Retirement planning is not just about money—it’s also about long-term discipline.

Successful retirement savers typically:

- Live below their means

- Save consistently

- Invest regularly

- Avoid emotional investing

- Review plans annually

- Adapt to changing circumstances

These habits contribute significantly to retirement success.

Conclusion

Retirement planning is one of the most important financial responsibilities you will ever undertake. The earlier you begin, the more opportunities you’ll have to build wealth, reduce financial stress, and create the retirement lifestyle you envision.

By setting clear goals, saving consistently, investing wisely, diversifying your portfolio, and planning for future expenses, you can build a secure financial foundation that supports you throughout retirement.

Remember that retirement planning is a lifelong journey. Small actions taken today can lead to a more comfortable, secure, and financially independent future tomorrow.